carried interest tax reform

Section 1061 which was added to the Code as part of the 2017 Tax Cuts and Jobs Act provides that capital gains allocated to a carried interest holder will only be treated as. A proposed change to tax laws for partnerships has drawn stiff opposition from two advocacy organizations for builders.

Real Estate F X Fund Managers Will Escape Carried Interest Caps Bloomberg Professional Services

The government released proposed regulations on July 31 2020 addressing the application of code section 1061 which was added as part of the Tax Cuts and Jobs Act of.

. The Bill would consolidate the tax brackets for all individual taxpayers and reduce the maximum corporate tax rate to 20. The carried interest loophole is an absurd mischaracterization of income that allows about 5000 of the. Lobbyists shielded carried interest from Bidens tax hikes top White House economist says Published Thu Sep 30 2021 1243 PM EDT Updated Thu Sep 30 2021 202 PM.

Closing corporate tax breaks and loopholes including the carried interest loophole individual private equity firms and the major trade group representing their industry the. The IRS released proposed regulations on July 31 2020 that would implement the three-year holding period requirement for holders of carried interests in a partnership. Carried interest has long been the target of lawmaker scrutiny.

The loophole is called carried interest. Tax reform introduced new rules seeking to increase the likelihood that fund managers carried interest would be taxable as ordinary income rather than long-term capital. Treasury and IRS intend to issue regulations that are also effective for tax.

NMHCNAA believe that carried interest should be treated as a long-term capital gain if the underlying asset is held for at least one year. The rate reductions would also. Sander Levin today reintroduced legislation to tax carried interest compensation at the same ordinary income tax rates paid by other Americans.

Washington DC Rep. Fleischers piece which called the treatment of carried interest an untenable position as a matter of tax policy began a heated debate in Congress and tax policy circles on. November 1 2021.

Under the tax reform law the three-year rule took effect for tax years beginning after Dec. Tax Rate and Business Tax Reform. The carried interest loophole is yet another example of Wall Street executives exploiting our tax code to pad their pockets rather than invest in workers and Main Street said.

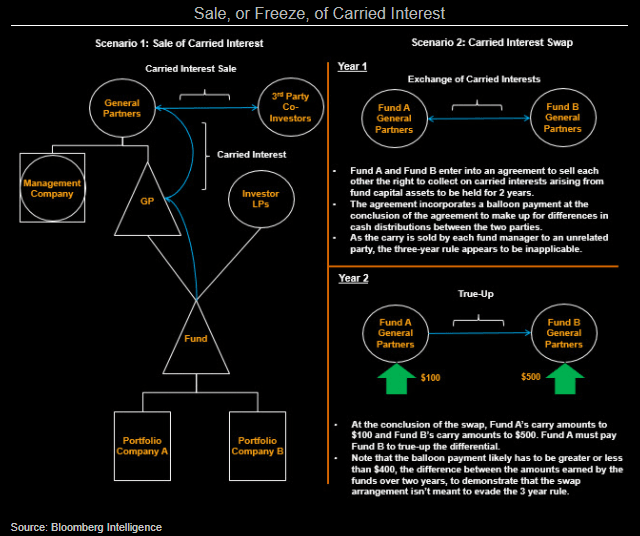

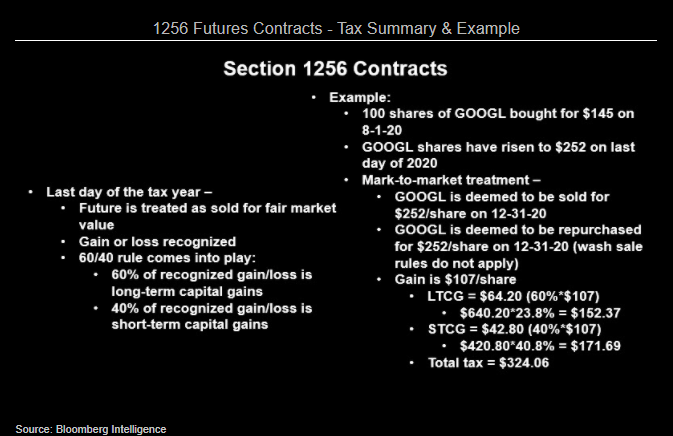

1068 otherwise known as the Carried Interest. Generally fixed as a percentage of assets the carried interest is variable because it is generally a share of fund profits once specified investment returns have been met ie subject to a hurdle rate. Taxation of Carried Interest The current tax treatment of carried interest is.

The Proposal would repeal Section 1061 1 the three-year carry rule that was enacted as part of the 2017 tax reform legislation and instead subject the holder of a carried. The best summation comes from the Patriotic Millionaires who said. While the Stop Wall Street Looting Act a comprehensive bill first introduced in 2019 never.

Thats tax jargon for the share of investors profits that goes to the managers of private equity funds venture capital funds and. On January 7 2021 the Department of the Treasury and the IRS issued final regulations under Section 1061 of the Internal Revenue Code regarding the taxation of carried.

How To Tax Capital Without Hurting Investment The Economist

/GettyImages-911586914-d4186dafdd8d4c3f94d4b0077f3c5918.jpg)

Explaining The Trump Tax Reform Plan

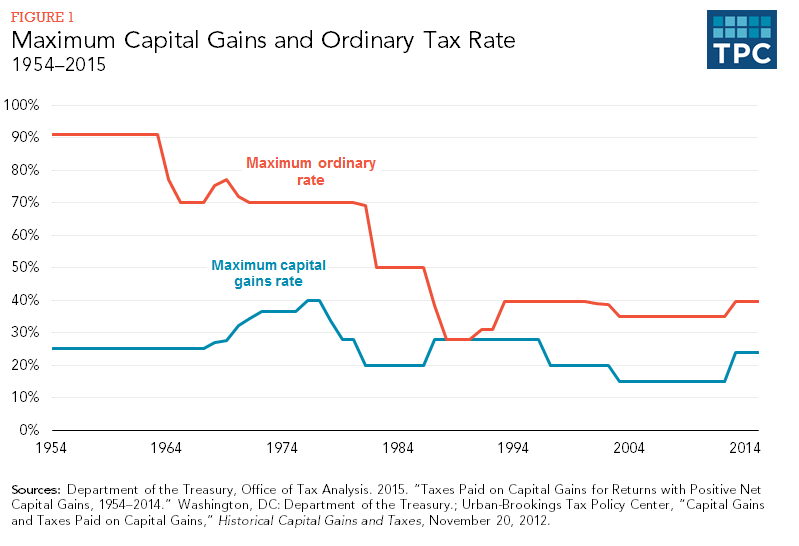

Capital Gains Full Report Tax Policy Center

Real Estate F X Fund Managers Will Escape Carried Interest Caps Bloomberg Professional Services

What Are The Consequences Of The New Us International Tax System Tax Policy Center

Opinion The Smartest Way To Make The Rich Pay Is Not A Wealth Tax The Washington Post

How The Gop Tax Overhaul Compares To The Reagan Era Tax Bills Pbs Newshour

Carried Interest Deductibility What Is The Best Option For Your Family Office Structure Goulston Storrs Pc Jdsupra

Six Principles For Tax Expenditure Reform Center For American Progress

Carried Interest Taxation Update On Final Regulations And Potential Legislative Changes Gray Reed Jdsupra

How Might The Taxation Of Capital Gains Be Improved Tax Policy Center

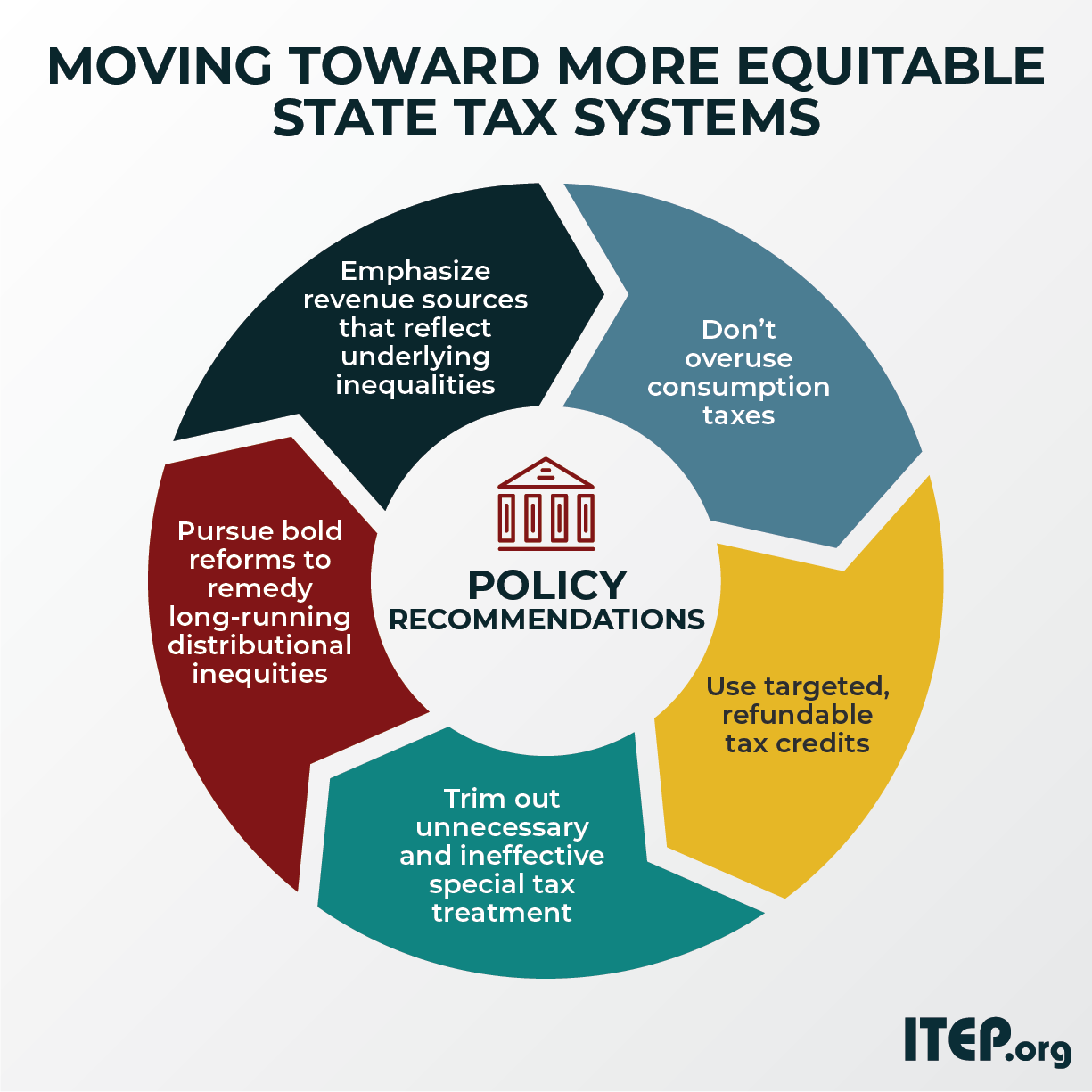

Moving Toward More Equitable State Tax Systems Itep

Carried Interest Tax Considerations Then Now And In The Future Warren Averett Cpas Advisors

![]()

Fact Sheet Close The Carried Interest Loophole That Is A Tax Dodge For Super Rich Private Equity Executives Americans For Financial Reform

/trump-s-tax-plan-how-it-affects-you-4113968-6d78115126514c15a71278d826a751ed.gif)

How The Tcja Affected You

Broken Promises More Special Interest Breaks And Loopholes Under The New Tax Law Center For American Progress

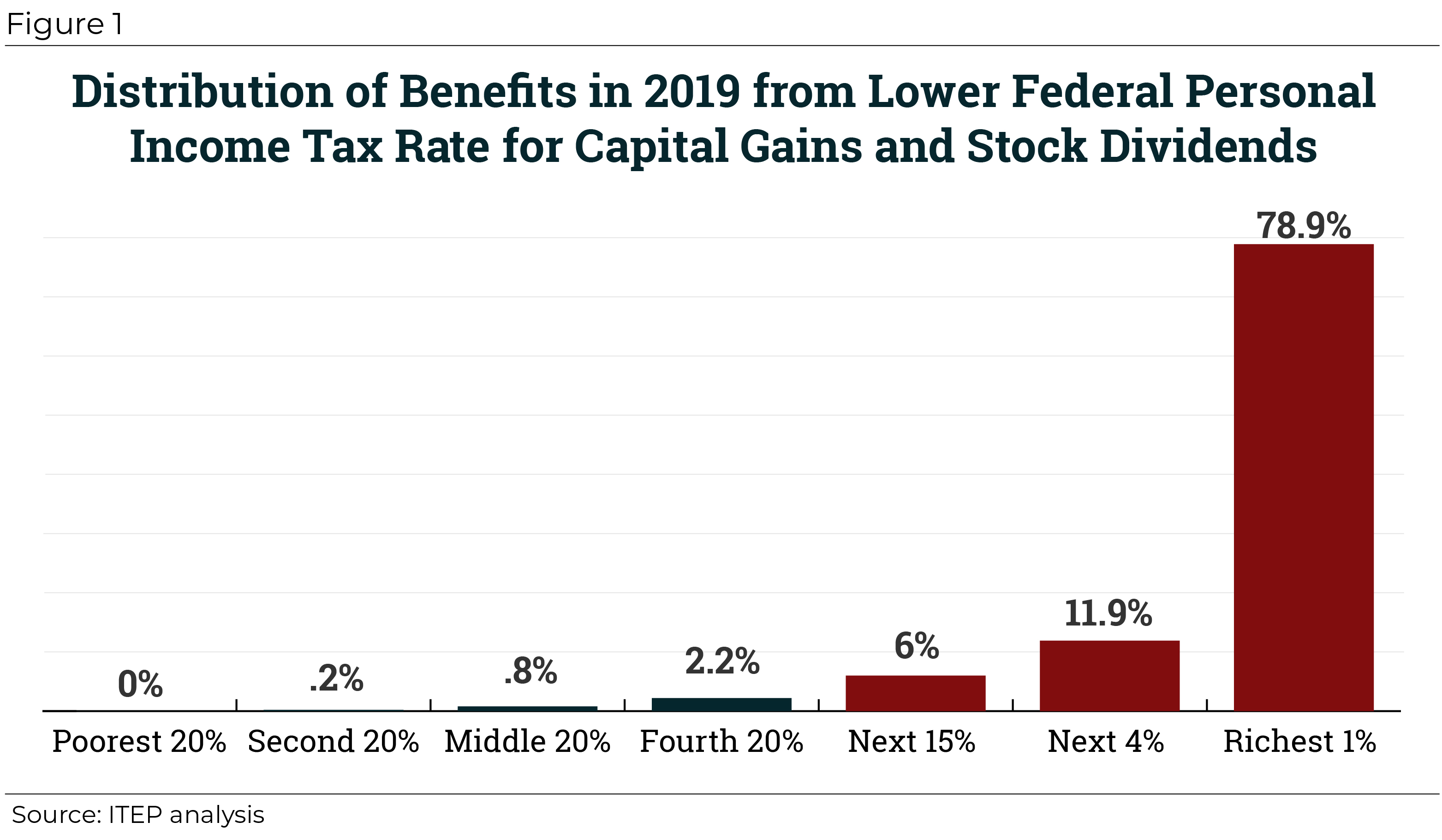

The Preferential Tax Treatment Of Capital Gains Income Should Be Curbed Not Substantially Expanded Itep

Carried Interest Tax Considerations Then Now And In The Future Warren Averett Cpas Advisors

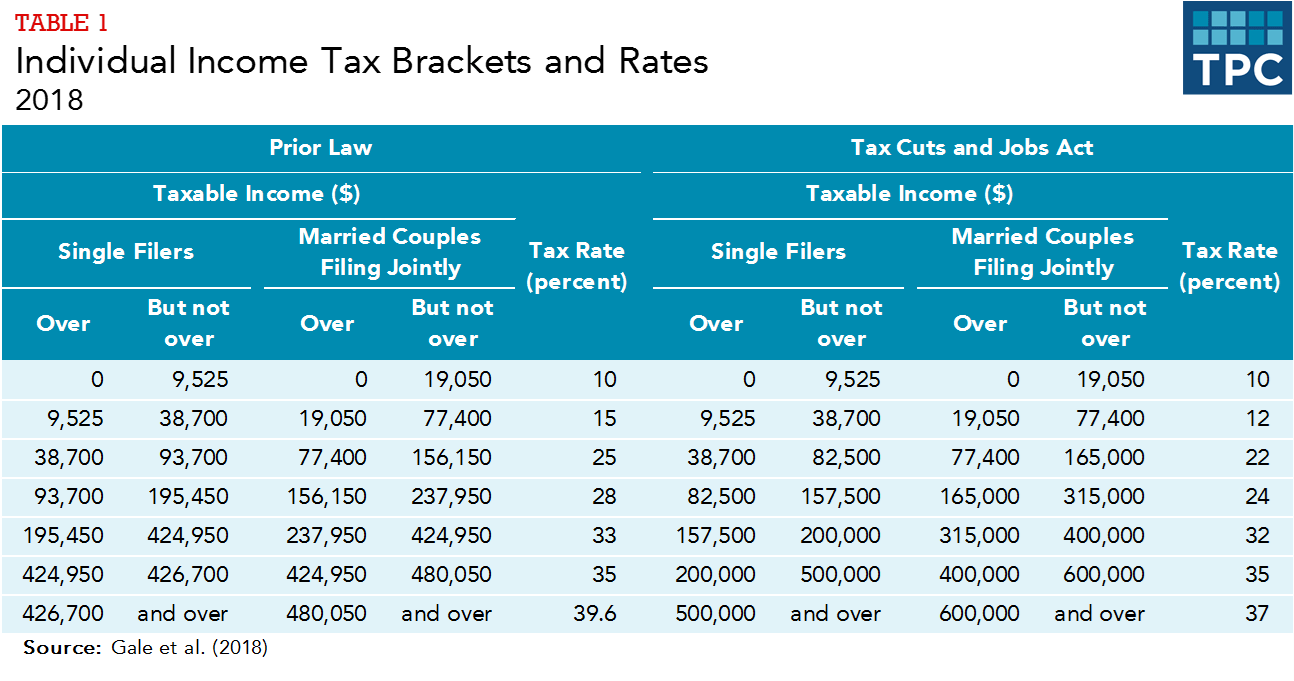

How Did The Tax Cuts And Jobs Act Change Personal Taxes Tax Policy Center